After a historically strong stretch for equities, the return of volatility tends to unsettle even seasoned investors. On Friday, June 5, the Nasdaq fell 4.2% — its largest single-day decline in a year. For ultra-high-net-worth families, the more useful question is not what the market did on a single day, but what the episode reveals about how a portfolio is built to weather it.

The pullback has clear, identifiable causes. Understanding them — and understanding why a diversified, family-office-style portfolio experiences days like this differently than a concentrated public-equity portfolio — is what separates a reaction from a strategy.

Why did the market pull back?

Counterintuitively, the decline followed a strong jobs report. Robust employment is good news for the economy, but it raises the possibility that the Federal Reserve could raise interest rates before year-end to keep inflation in check. A brief re-escalation of conflict in the Middle East added to the unease.

Notably, the bond market had been signaling this for some time. Yields have risen across the curve this year, with the 10-year Treasury near 4.5%. The bond market is often quicker than equities to price in the underlying realities of inflation, growth, and Fed policy — so it is not surprising that stocks, particularly interest-rate-sensitive ones, eventually reacted to the same signals. The lesson for long-term investors is that periods of strong returns are precisely when risk management and portfolio balance matter most, not least.

Why are technology stocks so sensitive to interest rates?

Investors buy technology and AI-related companies largely for growth expected far into the future, in contrast to established businesses with steady current cash flows. Because interest rates determine how those distant future profits are valued today, even small shifts in rate expectations — especially ones that change direction — can produce outsized swings. Rates act like a long lever: a modest move at one end creates a large effect at the other. This is the dynamic our note on tech stocks and higher interest rates explored in depth.

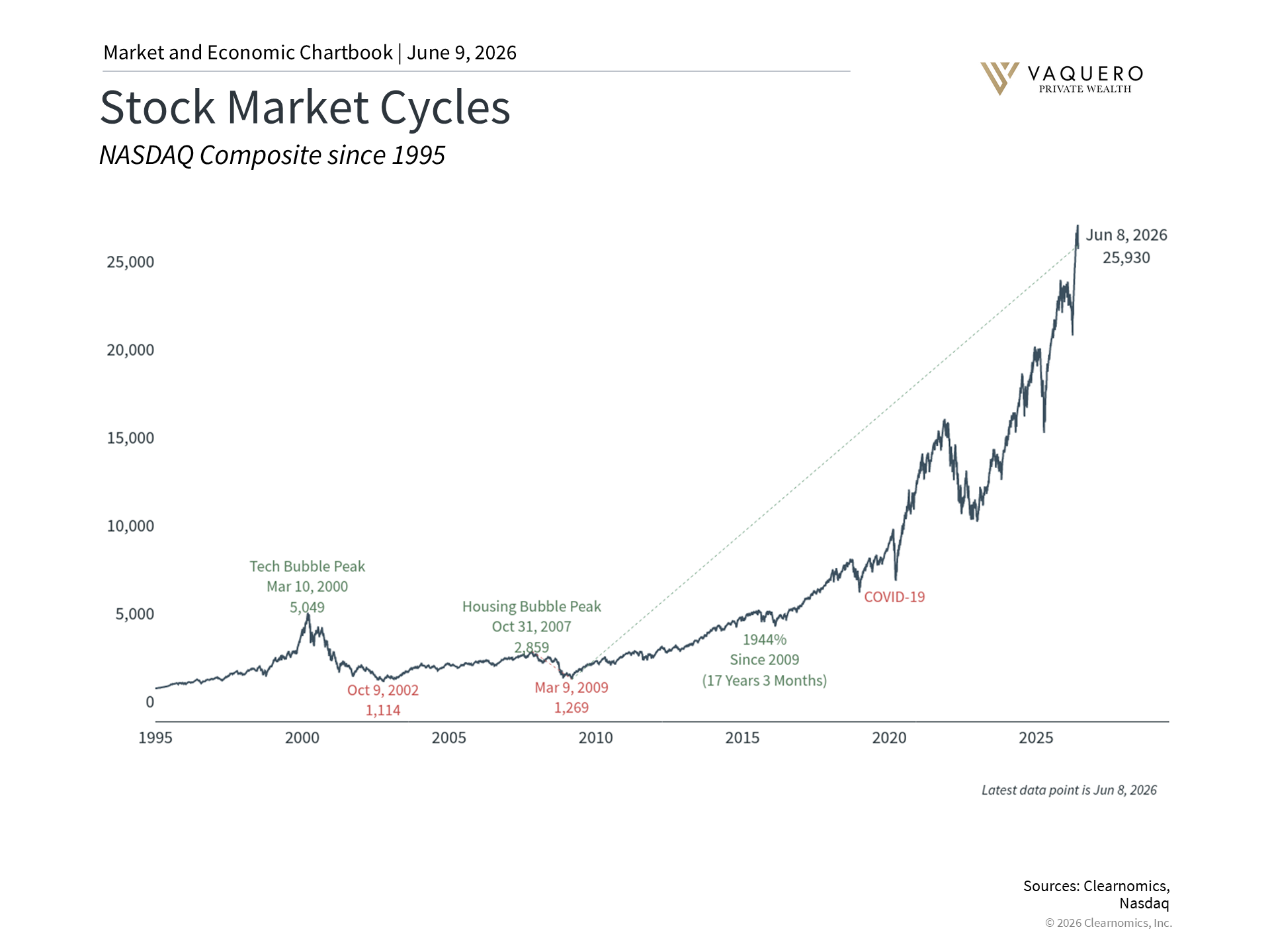

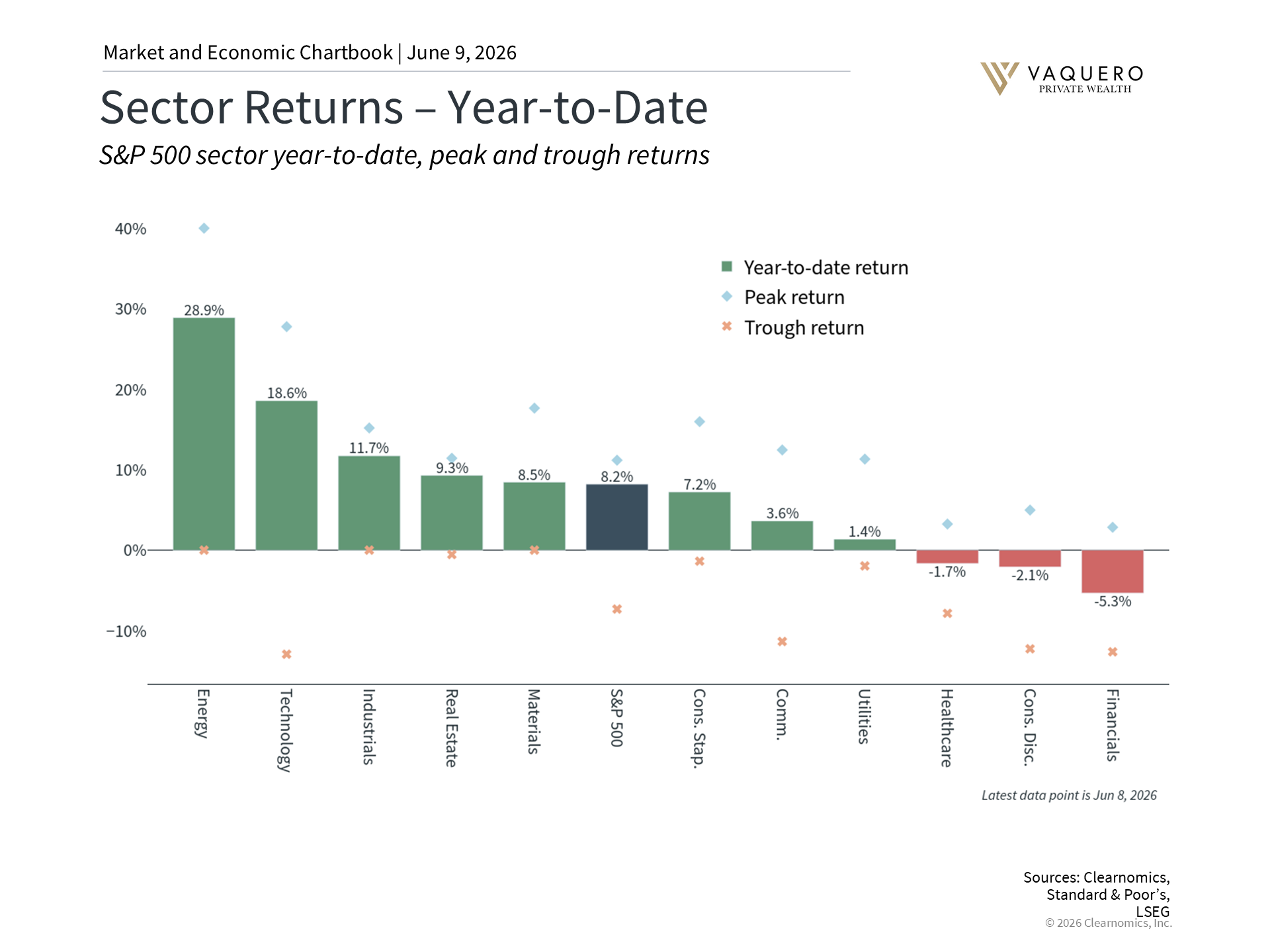

This matters more than it used to because technology now represents a far larger share of the market. The “Magnificent 7” — the largest technology names — now make up roughly one-third of the S&P 500. From their 2021 peak to their late-2022 trough, when inflation surged and rates jumped, this group lost about half its value before recovering to new highs. The practical implication for UHNW investors is concentration: anyone holding the index is now holding a heavily tech-weighted, rate-sensitive portfolio, often without intending to. Recognizing and managing that hidden concentration — as we did in our concentrated stock case study — is increasingly central to portfolio construction.

What would a Fed rate hike actually mean?

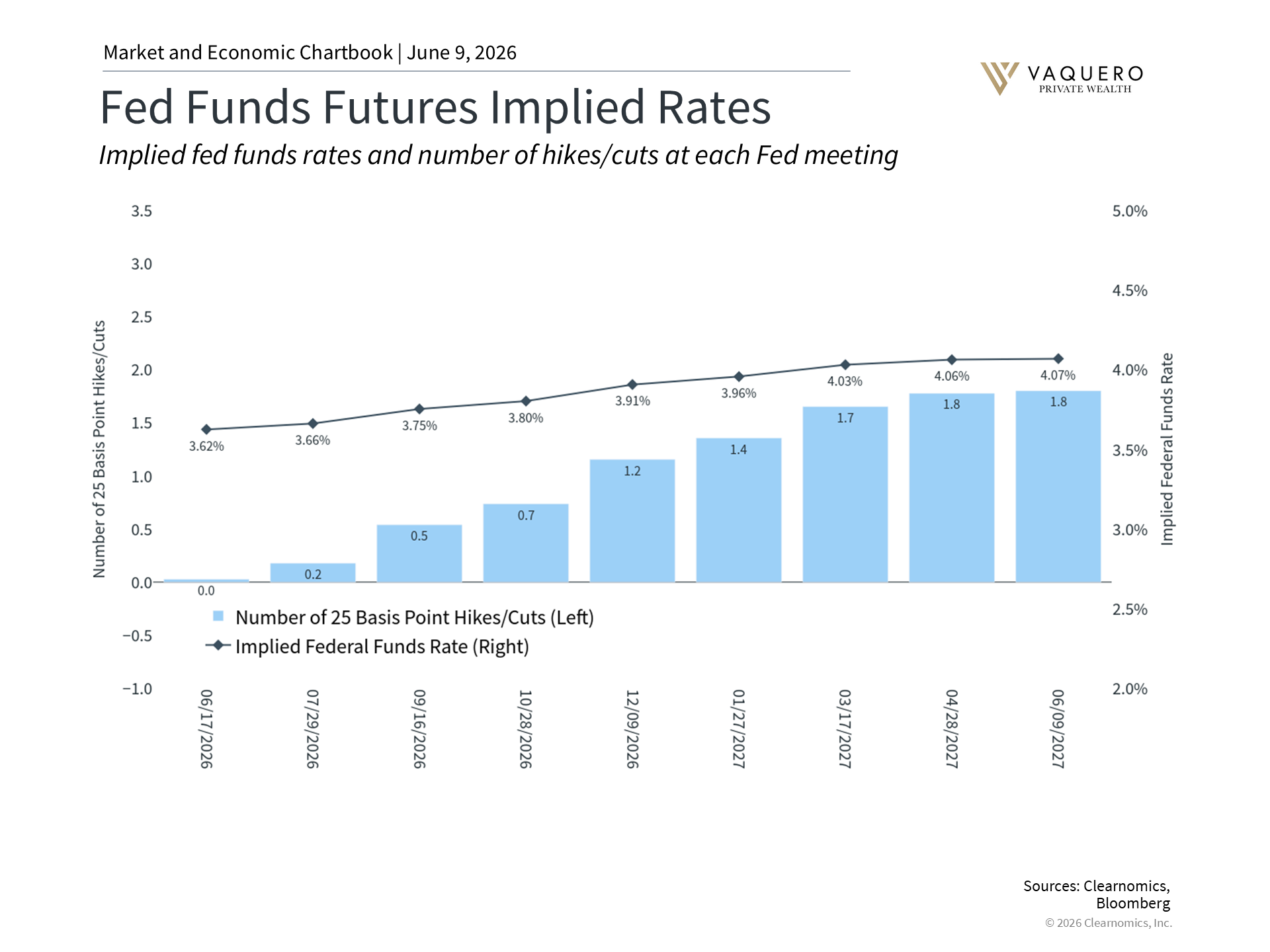

Expectations for Fed policy can shift quickly. Earlier this year the consensus expected continued rate cuts; that view reversed as energy prices rose and the labor market strengthened. There is also genuine uncertainty around how Kevin Warsh, as the new Fed chair, will approach inflation. He has historically been viewed as an inflation hawk and has argued the Fed should reduce its balance sheet — both of which point toward tighter conditions.

Even so, perspective is essential. Markets currently anticipate at most a single 25-basis-point hike by year-end — modest by any historical standard, and a fraction of the 2022–2023 cycle, when the Fed raised rates from near zero to 5.25% across eleven hikes. More importantly, equities have historically performed well across many different rate environments, including periods of rising rates — particularly when the Fed is tightening because the economy is genuinely strong, which tends to support corporate earnings.

How do private investments behave during public-market volatility?

This is where the experience of an ultra-high-net-worth portfolio diverges most from a conventional one. For a family whose wealth sits entirely in public equities, a day like June 5 is felt immediately and in full. For a family that allocates across public and private markets — the approach most single- and multi-family offices take — the day is felt differently.

The reason is genuine diversification — not a quirk of how private assets are reported, but the fact that they earn their returns from fundamentally different economic engines than public technology stocks. When the Nasdaq drops on a shift in rate expectations, it is reacting to a single dominant force. The private holdings in a well-constructed family-office portfolio are, by design, not tethered to that same force.

Consider the return drivers behind the kinds of private investments a family office assembles. Multi-family real estate development turns on housing demand, rents, and execution. Litigation finance depends on the resolution of legal cases — returns with essentially no relationship to the Federal Reserve or the level of the Nasdaq. Toll road equity is driven by traffic volumes and contracted, often inflation-linked toll escalators. Energy exploration and production moves with commodity prices and supply. None of these track technology-stock valuations — and energy, in particular, can act as a counterweight in precisely the inflationary, rising-rate environment that pressures growth equities. Assembling a basket of these uncorrelated return streams is what real diversification looks like: the portfolio stops rising and falling on any single factor.

The tradeoff is liquidity. Private commitments carry capital calls and lock-ups, which is why a disciplined family-office allocation always pairs private exposure with a deliberate liquidity sleeve — cash and liquid assets sized to meet capital calls, fund spending, and act opportunistically when public markets dislocate. Approached this way, volatility is not only a risk to be managed; for a well-structured portfolio with dry powder, it can be a source of opportunity.

What should UHNW families do now?

Very little that is reactive, and a great deal that is structural. The families who navigate volatility best are not the ones who predict it — they are the ones whose portfolios were built in advance to absorb it: diversified across public and private markets, deliberate about concentration and rate sensitivity, and paired with the liquidity to stay invested and opportunistic when others are forced to sell. That preparation is the work of calm markets, not volatile ones. If your allocation hasn't been reviewed through this lens recently, now — while markets are still near highs — is the right time. We're always glad to begin a confidential conversation.

The bottom line

Recent volatility reflects the real possibility of Fed rate hikes and renewed geopolitical tension — but neither is a reason to abandon a sound long-term plan. History shows markets can perform well across many rate cycles. And for ultra-high-net-worth families, a thoughtfully diversified, family-office-style allocation — spanning public and private markets with disciplined liquidity — is what turns episodes like this from a source of anxiety into a test the portfolio was already built to pass. For our broader read on conditions, see our latest market update.

If recent volatility has you reconsidering how your portfolio is built, schedule a conversation with our team.

This commentary was prepared by Vaquero Private Wealth and reflects the authors' current opinions, which are subject to change without notice. It is based on sources believed to be accurate and reliable but is not a solicitation, recommendation, or an offer to buy or sell any security. Past performance is not a guide to future results. Private investments involve illiquidity and other risks and are not suitable for all investors.

Underlying market data and charts adapted from Clearnomics, Inc. Sources include the CME FedWatch Tool and the U.S. Department of the Treasury.