April’s market performance is a reminder that strong gains can occur even during periods of elevated uncertainty. Despite ongoing geopolitical tensions in the Middle East, major equity markets climbed to new all-time highs during the month.

The S&P 500 rose 10.4% in April alone, marking one of its strongest monthly performances in history. While this rebound may seem surprising, similar recoveries have occurred during past episodes of market stress.

Key Market and Economic Drivers in April

- The S&P 500 and Nasdaq gained 10.4% and 15.3%, respectively, while the Dow Jones Industrial Average rose 7.1%.

- Market volatility declined, with the VIX Index falling from 25.3 to 16.9.

- International developed and emerging markets posted strong gains.

- U.S. small- and mid-cap stocks outperformed large caps.

- The 10-year Treasury yield finished the month near 4.37%, while bond returns were relatively flat.

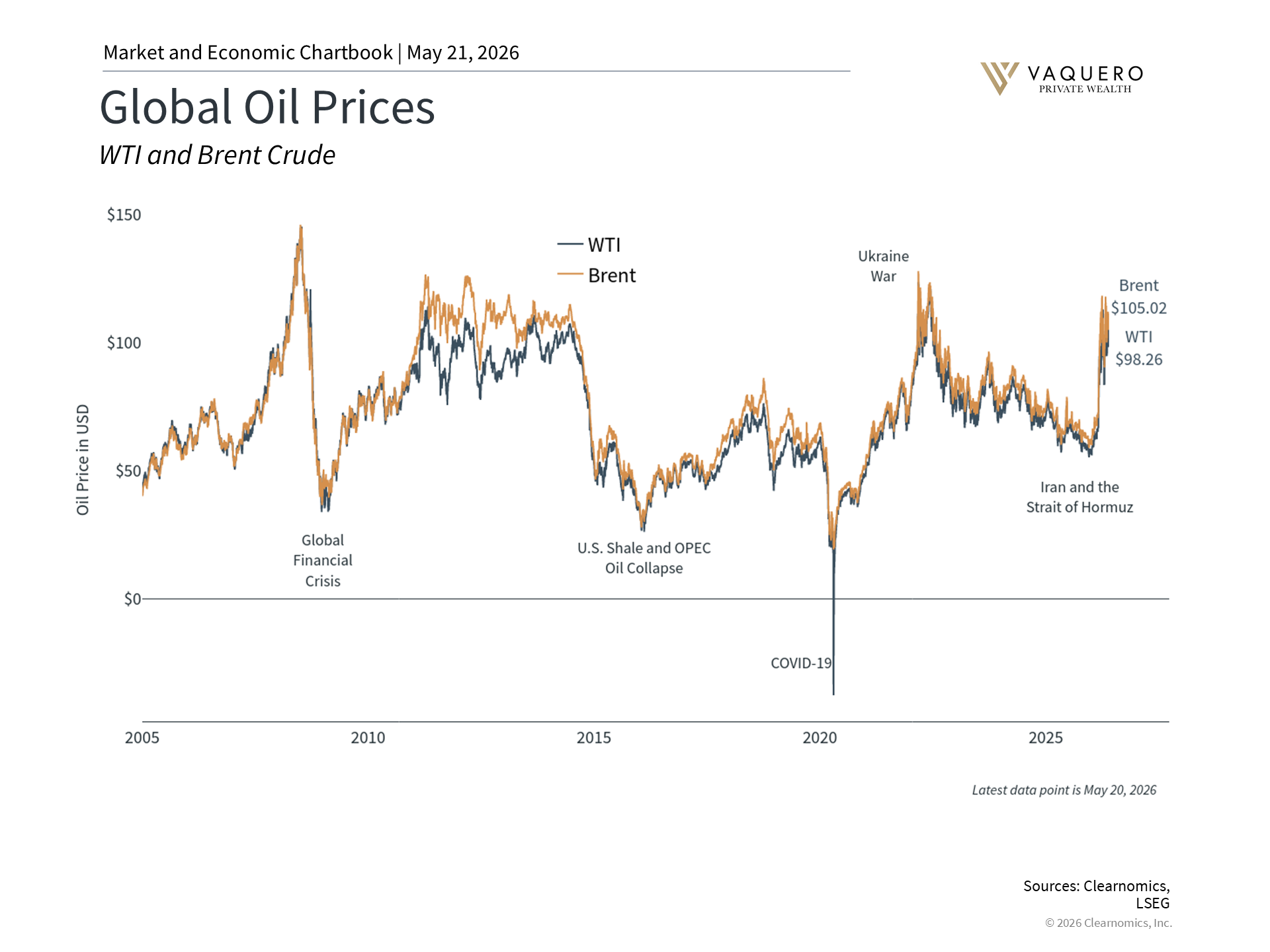

- Oil prices remained volatile as the Strait of Hormuz stayed closed to shipping.

- Gold prices and the U.S. dollar both declined modestly during the month.

The Stock Market Rebound

Historically, some of the strongest market months have occurred when investor sentiment was most cautious. This pattern has repeated after major disruptions such as the 2020 pandemic, the inflation-driven downturn of 2022, and the tariff-related volatility of 2025.

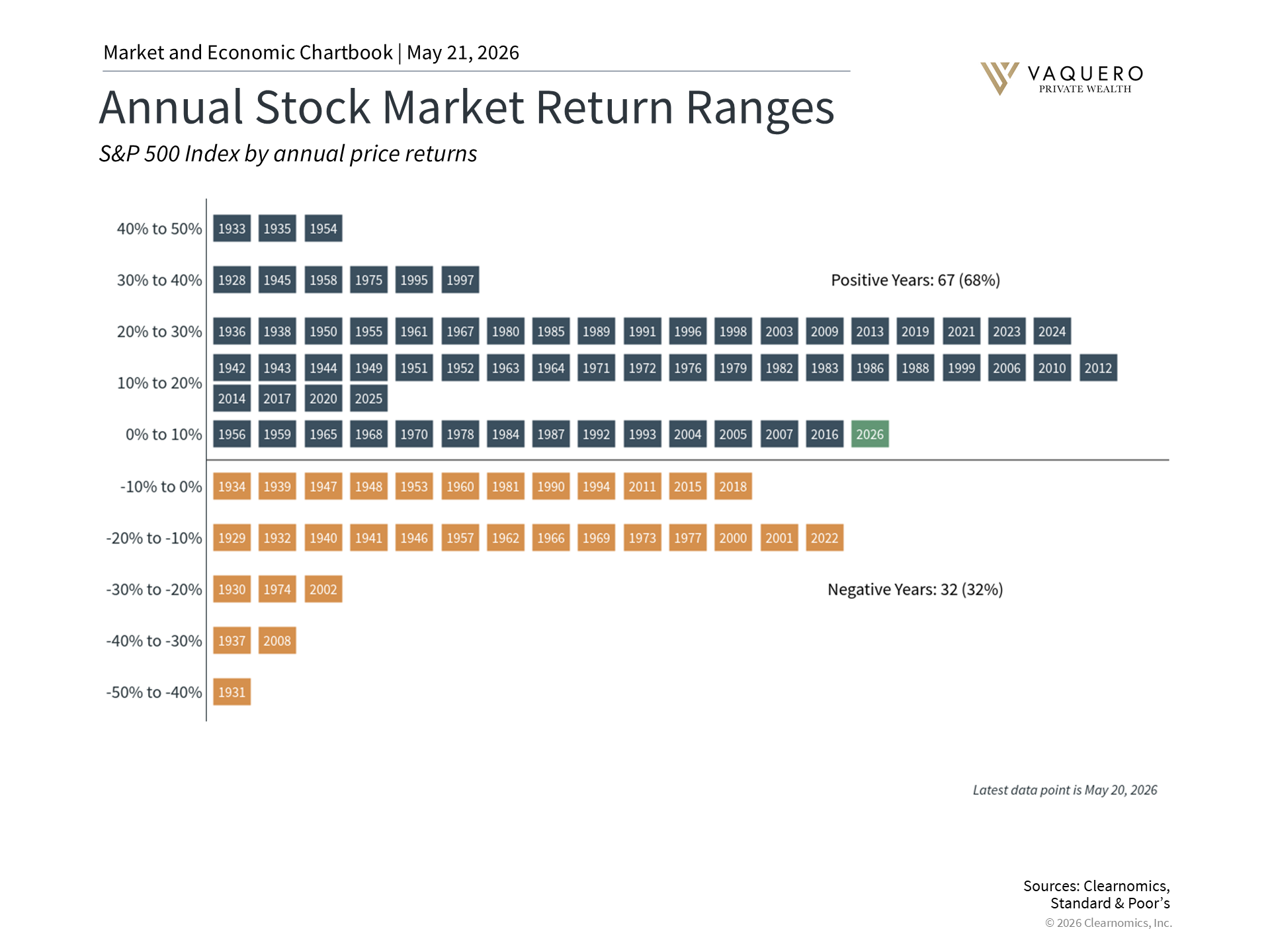

When combined with losses earlier in the year, the S&P 500 is now modestly positive year-to-date. Over long periods, markets have delivered positive returns in the majority of years, underscoring the challenge of timing market movements.

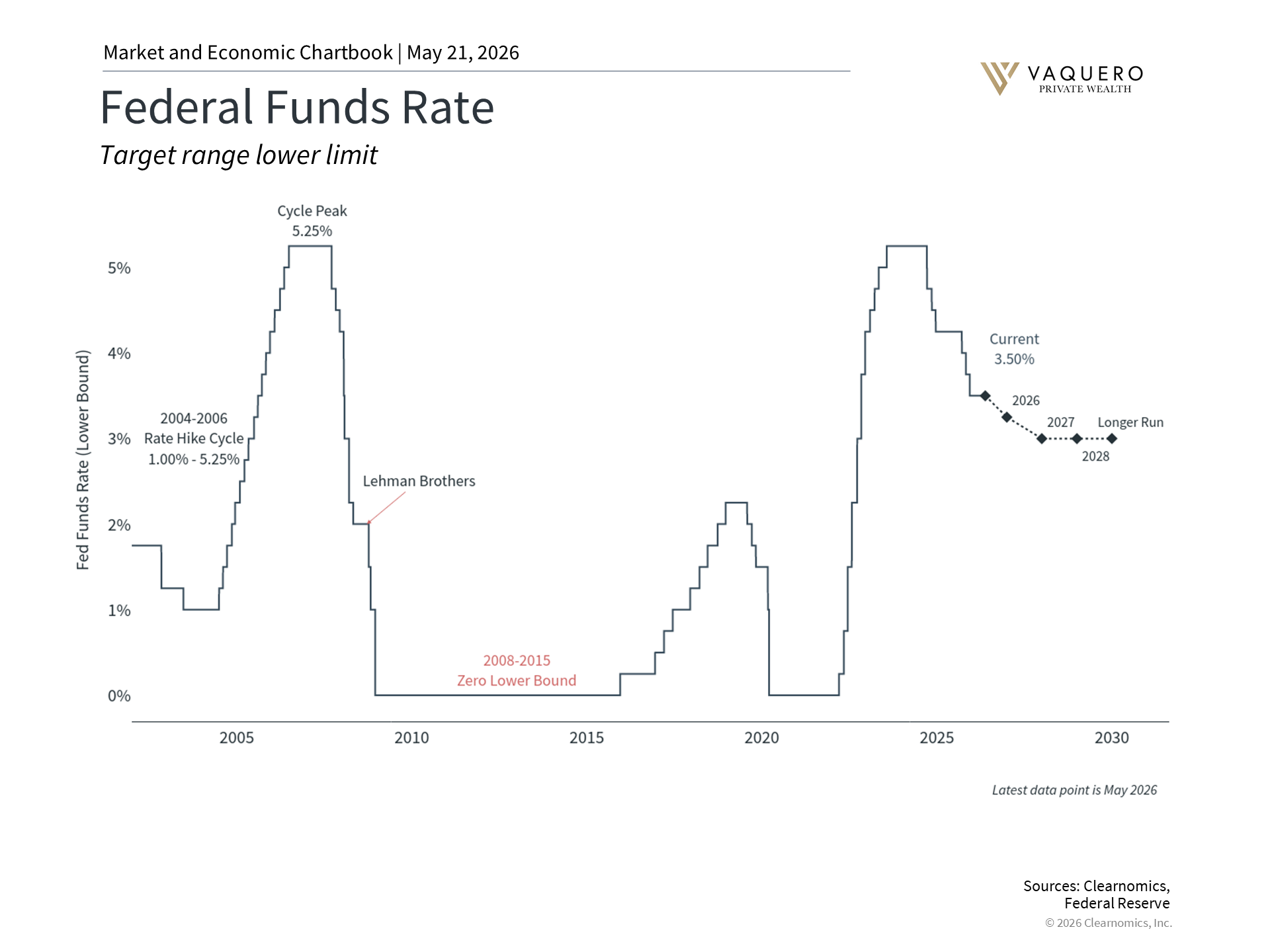

Federal Reserve Policy and Leadership Transition

The Federal Reserve held its policy rate steady in April, though internal disagreement among committee members highlighted the complexity of balancing inflation risks against signs of labor market softening. As rates remain elevated, investors may also consider the portfolio implications of higher interest rates alongside trends in tech stocks and IPO activity.

April also marked the final policy meeting under Chair Jerome Powell. While leadership changes introduce uncertainty, markets and the economy have historically adapted across many monetary policy regimes.

Oil Prices and the Strait of Hormuz

Oil prices remained elevated as disruptions in the Strait of Hormuz continued to constrain global supply. While higher energy costs can pressure inflation, history suggests these effects often fade as conditions stabilize.

The U.S. remains the world’s largest producer of oil and natural gas, providing a degree of insulation compared to prior decades.

The Bottom Line for Investors

April’s rebound demonstrates that markets can move higher even during challenging environments. A diversified, long-term investment strategy is designed to navigate uncertainty rather than react to short-term headlines. The positive momentum continued into May; read our May 2026 market update for the latest on record highs, interest rates, and the Fed transition. For families with multi-generational wealth, estate planning is an equally important component of long-term financial resilience. See our advanced estate planning strategies for a deeper look at how to structure wealth transfers across generations.